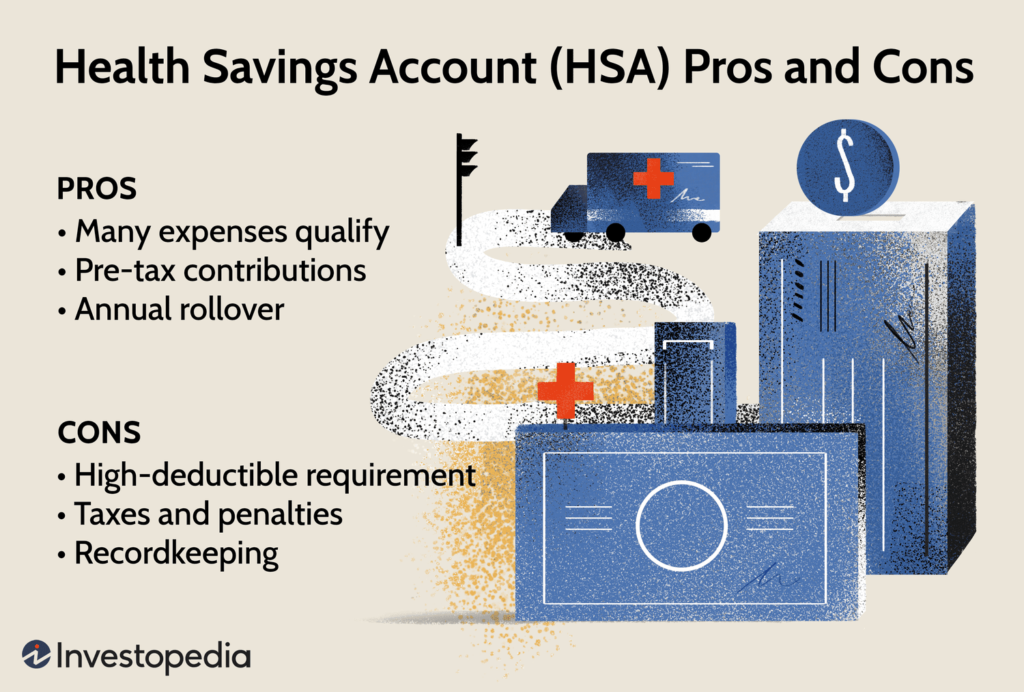

Health Savings Accounts (HSAs) are becoming increasingly popular as individuals seek ways to manage their healthcare costs more effectively. These accounts offer a unique blend of tax advantages and flexibility for those enrolled in high-deductible health plans (HDHPs).

However, like any financial tool, HSAs come with their own set of advantages and disadvantages. This article will explore the various pros and cons of HSAs, providing a comprehensive overview to help individuals make informed decisions.

What is a Health Savings Account (HSA)?

A Health Savings Account (HSA) is a tax-advantaged account designed to help individuals save for medical expenses. To qualify for an HSA, one must have a high-deductible health plan (HDHP). The funds in an HSA can be used to pay for a wide range of qualified medical expenses, from routine visits to more significant healthcare needs.

Key Features of HSAs

- Tax Advantages: Contributions to HSAs are made with pre-tax dollars, reducing taxable income. Additionally, any interest or investment gains on the account are tax-free, and withdrawals for qualified medical expenses are also tax-free.

- Portability: HSAs are owned by the individual, meaning they remain with you even if you change jobs or insurance plans.

- Contribution Limits: As of 2024, the contribution limits for HSAs are $3,850 for individuals and $7,750 for families, with an additional catch-up contribution of $1,000 for individuals aged 55 and older.

Pros of Health Savings Accounts

1. Tax Benefits

One of the most significant advantages of HSAs is the triple tax benefit they offer:

- Pre-tax Contributions: Contributions reduce your taxable income, leading to immediate tax savings.

- Tax-Free Growth: Any interest or investment earnings on the HSA balance grow tax-free.

- Tax-Free Withdrawals: Withdrawals for qualified medical expenses are not taxed, making HSAs an efficient way to manage healthcare costs.

2. Flexibility in Spending

HSAs provide flexibility in how and when you spend your funds. You can use the money in your account for a wide variety of qualified expenses, including:

- Doctor visits

- Prescription medications

- Vision care

- Dental services

This flexibility allows individuals to manage their healthcare costs in a way that suits their personal needs.

3. Roll Over and Accumulate Funds

Unlike Flexible Spending Accounts (FSAs), which may require you to use funds by the end of the year, HSAs allow you to roll over unused funds year after year. This feature enables account holders to accumulate savings for future medical expenses, making HSAs an attractive option for long-term healthcare planning.

4. Investment Opportunities

Many HSAs offer the option to invest funds in various investment vehicles, such as stocks, bonds, or mutual funds, once the balance exceeds a certain threshold (often $1,000). This investment potential can lead to significant growth over time, making HSAs not only a savings account but also a long-term investment tool for healthcare expenses.

5. Portability

HSAs are individually owned accounts, meaning they are not tied to an employer. If you change jobs or retire, your HSA remains with you. This portability is particularly beneficial for individuals who may change their insurance plans or jobs frequently.

6. Family Contributions

HSAs also allow for contributions from family members or employers, which can help build the account balance more quickly. This feature is particularly useful for families managing multiple medical expenses.

Cons of Health Savings Accounts

1. Requirement for High-Deductible Health Plans

To qualify for an HSA, individuals must be enrolled in a high-deductible health plan (HDHP). While HDHPs typically have lower premiums, they also come with higher deductibles that can lead to significant out-of-pocket costs before the insurance kicks in. This requirement may not be suitable for everyone, especially those who frequently use medical services.

2. Potential for Limited Contributions

The contribution limits for HSAs may be restrictive for some individuals or families, particularly those facing high medical expenses. While the limits are adjusted annually, they may not keep pace with soaring healthcare costs, leaving some individuals underfunded.

3. Not Ideal for Immediate Needs

For individuals who require immediate medical care or have ongoing healthcare expenses, an HSA may not be the best option. The high deductible associated with HDHPs may lead to significant out-of-pocket costs before the insurance coverage begins, which can be burdensome for those with limited savings.

4. Complexity in Managing Funds

Managing an HSA can be complex, particularly when it comes to understanding which expenses are qualified and how to maximize tax benefits. This complexity may deter some individuals from fully utilizing their HSAs or lead to errors in spending.

5. Investment Risks

While investing HSA funds can lead to growth, it also comes with risks. The value of investments can fluctuate, and there is a potential for loss. Individuals need to be comfortable with these risks and have a good understanding of investment principles to make informed decisions.

6. Penalties for Non-Qualified Withdrawals

If funds are withdrawn for non-qualified expenses before age 65, a 20% penalty applies, in addition to regular income tax. This penalty can be a significant deterrent for those considering HSAs, particularly if they anticipate needing to access funds for non-medical purposes.

Conclusion

Health Savings Accounts (HSAs) offer a unique blend of tax advantages, flexibility, and long-term savings potential for those enrolled in high-deductible health plans. While they provide several benefits, including tax savings, investment opportunities, and portability, they are not without their drawbacks. Individuals must carefully consider their healthcare needs, financial situation, and comfort with high-deductible plans before opting for an HSA.

As healthcare continues to evolve and costs rise, HSAs may become an increasingly important tool for managing medical expenses. However, understanding both the pros and cons is essential for making informed decisions that align with one’s financial and health care goals.