Understanding Medicare Late Enrollment Penalties – As individuals approach retirement age, understanding Medicare becomes increasingly important. One of the critical aspects of Medicare enrollment is the potential for late enrollment penalties.

These penalties can significantly affect the cost of healthcare for seniors who do not enroll during their Initial Enrollment Period (IEP). This article will explore the implications of late enrollment in Medicare, the types of penalties involved, and strategies to avoid them.

What is Medicare?

Medicare is a federal health insurance program primarily designed for individuals aged 65 and older, although it also serves younger individuals with disabilities or specific diseases such as end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS). Medicare is divided into various parts:

- Part A (Hospital Insurance): Covers inpatient hospital stays, skilled nursing facility care, hospice, and some home health care.

- Part B (Medical Insurance): Covers outpatient care, preventive services, ambulance services, and some home health care.

- Part C (Medicare Advantage): A private insurance plan that bundles Parts A and B, often including additional benefits.

- Part D (Prescription Drug Coverage): Provides prescription drug coverage through private insurance plans.

Each part of Medicare has its own enrollment periods and rules, making it essential for beneficiaries to understand when and how to enroll to avoid penalties.

Types of Late Enrollment Penalties

When individuals do not enroll in Medicare during their IEP, they may face penalties that can lead to higher premiums for the duration of their enrollment. The penalties differ based on the specific part of Medicare:

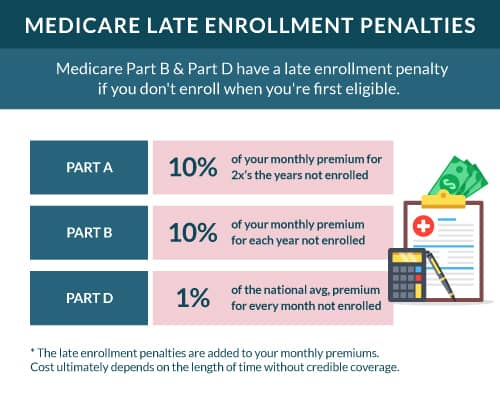

Part A Late Enrollment Penalty

Most individuals do not pay a premium for Part A if they or their spouse paid Medicare taxes for at least 10 years. However, if a person decides to delay enrolling in Part A and is not eligible for premium-free Part A, they may face a penalty. The penalty consists of a premium increase of 10% for twice the number of years they could have enrolled but did not. This increased premium applies for twice the number of years they delayed enrollment.

Part B Late Enrollment Penalty

For Part B, the penalty is calculated as an increase of 10% for each full 12-month period that an individual could have enrolled in Part B but did not. For example, if someone delays enrollment for three years, their Part B premium could be increased by 30% for as long as they are enrolled in Medicare. Given the base premium of $174.70 in 2024, a penalty could raise the premium to approximately $226.11 monthly if calculated over three years.

Part D Late Enrollment Penalty

The late enrollment penalty for Medicare Part D is a little more complex. It is calculated by taking 1% of the national base beneficiary premium ($34.70 in 2024) for each full month that an individual was eligible for Part D but did not enroll and did not have creditable prescription drug coverage. For instance, if a person waited 14 months to enroll, they would incur a penalty of 14% on the current premium, which translates to an additional cost on top of their monthly premium.

How Penalties are Calculated

- Part B: If an individual delays enrollment for 3 years, their monthly premium would be 30% higher than the standard premium. If the standard premium is $174.70, the penalty would mean a monthly cost of approximately $226.11.

- Part D: If an individual was without creditable prescription drug coverage for 14 months, their penalty would be calculated as follows:

- 1% of the national base beneficiary premium ($34.70) = $0.347.

- Multiply this by the number of months without coverage (14 months): $0.347 x 14 = $4.86.

- This means that the monthly premium for Part D would be increased by $4.86.

Why Late Enrollment Penalties Exist

The rationale behind late enrollment penalties is to encourage timely enrollment in Medicare. When individuals delay enrollment, it can lead to higher healthcare costs for the Medicare program overall, as those who wait may be less healthy when they finally enroll. Penalties act as a deterrent against delaying enrollment, ensuring that beneficiaries take advantage of the program when they are eligible.

Exemptions and Special Circumstances

There are specific scenarios where individuals may not face late enrollment penalties. These include:

- Creditable Coverage: If individuals had other health insurance coverage that is considered “creditable” (meaning it is as good as Medicare), they may avoid penalties if they enroll in Medicare after that coverage ends.

- Special Enrollment Periods (SEPs): Certain life events, such as moving, losing other health coverage, or qualifying for Medicaid, can grant individuals a Special Enrollment Period, allowing them to enroll in Medicare without facing penalties.

Strategies to Avoid Late Enrollment Penalties

- Understand Enrollment Periods: Familiarize yourself with the Initial Enrollment Period, General Enrollment Period, and Special Enrollment Periods. Mark important dates on your calendar to ensure you don’t miss them.

- Assess Other Coverage: If you have other health insurance, confirm whether it is considered creditable coverage. If it is, keep documentation, as you may need this when you enroll in Medicare.

- Consult with Experts: Consider speaking with a Medicare expert or a licensed insurance agent who can guide you through the enrollment process and clarify any questions regarding potential penalties.

- Stay Informed: Regularly check resources such as the official Medicare website or local Medicare offices to stay up to date on any changes to policies or penalties.

Conclusion

Late enrollment in Medicare can lead to significant financial penalties that impact seniors’ healthcare costs over time. Understanding the types of late enrollment penalties associated with Parts A, B, and D is crucial for anyone approaching Medicare eligibility. By staying informed and planning accordingly, individuals can avoid these penalties and ensure they receive the benefits they need in a timely manner. As the healthcare landscape continues to evolve, being proactive about Medicare enrollment becomes increasingly important for financial and physical well-being in retirement.